Agriculture: Part of the Solution not the Problem - Agri Feedstocks and Sustainable Aviation Fuel

Thu 12 Dec 2024

With the overall drive towards decarbonisation – the airline industry faces major hurdles in how emissions are going to be cut. Whilst greenhouse-gas emissions are not huge at 2% - they are growing fast and the International Civil Aviation Organisation, an arm of the UN, forecasts that such emissions could rise between three and seven fold by 2050 if nothing substantial is done.

Pressured by climate change and committed to 2050 net zero, the EU and US have passed regulations and incentives to make the industry more sustainable, actions include: tax credits for R&D; framework for carbon counting and reporting; and regulating and recognising carbon offsetting. However, most importantly, regulations on the percentage content of SAF (Sustainable Aviation Fuel) within the total aviation fuel mix have been adopted by the UK and EU and the US is offering tax credits of up to $1.75 per gallon of SAF that achieves at least 50% reduction in greenhouse-gas emissions.

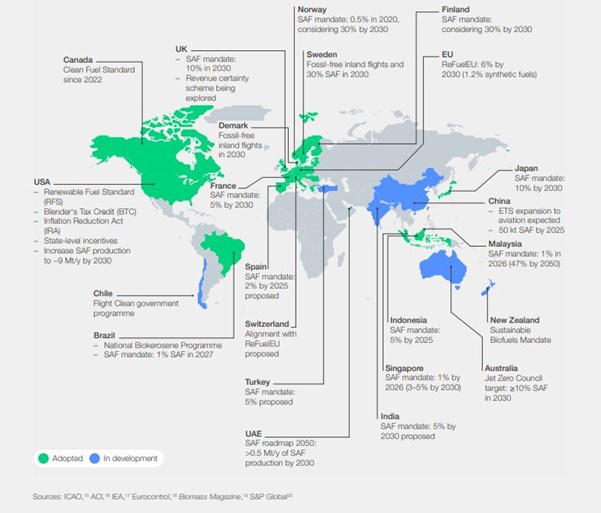

Global Policies moving towards SAF

SAF is making its way into government policy across the globe, although with small initial commitments. The following map (sourced from World Economic Forum, 2024) shows policy adopted or in progress in different countries.

Current SAF Production

Current SAF production is estimated to be 1.9 billion litres (IATA), which represents a tiny 0.53% of fuel demand for 2024. Raw materials used include food by products or waste products such as Used Cooking Oil (UCO). Brown & Co participated in a project in Egypt in 2024 looking at UCO feedstock supply and existing supply side challenges and it is largely recognised that UCO feedstock supply will only provide a drop in the ocean compared to the tidal wave of demand coming as the industry grows the inclusion rate up towards 70% in 2050.

Role of Ag - Feedstocks

In the short and medium term crops such as corn, soybeans and rapeseed are likely to receive attention and in the U.S. are currently being used as feedstock for SAF. In the EU there are non-food and non-feed crop requirements to meet the sustainability criteria which means cover crops and biomass are now likely medium term feedstock candidates. The UN body, ICAO divides feedstock into primary and co-products (e.g. Corn, Rapeseed oil, Sugar Beet, Miscanthus), by-products (e.g. poultry fat), wastes (e.g. municipal solid waste) and residues such as straw and forestry residues. Other crops are also receiving a lot of attention and experiments and crop development is gathering pace with crops such as: camelina, jatropha, carinata, and pongamia. These crops offer a number of advantages such as being used as cover crops, providing windbreaks, offering shade, creating green corridors, and enhancing biodiversity. Many of these crops are capable of growing in marginal fields with low nutrient levels or in areas with dry conditions that would otherwise be classified as marginal land.

Developing Production and Supply Chains

Ideal feedstock growing conditions include favourable climate, land availability and scale, and low costs of production given that SAF is currently two to three times more expensive than conventional fuel (SAF 2,437 USD vs Conventional 1, 094 USD – at Sep 2023). Responsible production and traceability are important and the goal is to use feedstocks that have minimal impact on the environment, are cost-effective, and do not compete with food resources which is contentious as SAF cannot be competing for land used for food production.

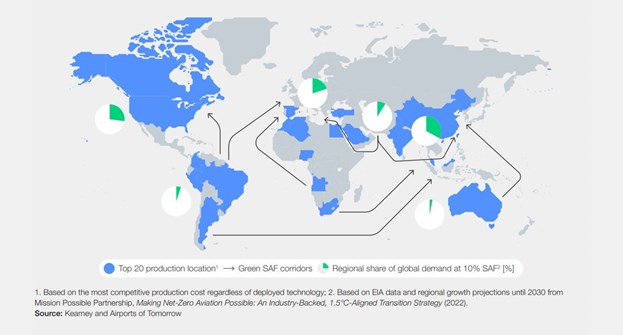

The World Economic Forum recognized 20 countries with favourable SAF production potential, four countries in South America (Peru, Colombia, Argentina, and Brazil); six Countries in Africa (Angola, South Africa, Morocco, Algeria, Egypt and Nigeria). Other countries include China, India, US, Canada and Australia although these countries will face higher costs of production and could still rely on imports given their air traffic concentration.

Miscanthus giganteus plants being grown for biofuel on a Dutch farm.

Miscanthus giganteus plants being grown for biofuel on a Dutch farm.

Land – Energy – Water – Climate: the Road ahead

The net zero 2050 goal is clear, and policy is evolving, yet it will take time to bring together the different players involved: the aviation sector, crop researchers, engineers, policy makers and agricultural sector.

Feedstock production will have to scale and therefore it is likely to be met by a diverse range of types and sources. Costs of production, logistics and infrastructure will be key and “real world” joined up thinking will be required to move from theory to practice to implementation. In terms of agriculture, the opportunity to contribute to a sustainable aviation sector is considerable, but farmers must be informed/educated and supported. If managed correctly farmers may see feedstock for SAF as added value on practices that they are already engaged with: government sustainability schemes, supplying anaerobic digesters or producing cover crops.

Regulation is essential to ensure a level playing field among suppliers and to guarantee traceability throughout the supply chain in order to guarantee sustainability credentials rather than so much of the green washing present in other sectors. It is also crucial to protect food safety, making sure that production of SAF does not compete with food supply.

Finally, policy must be proactive, fostering and developing a system that addresses all these aspects, while ensuring SAF is both available and economically viable. By encouraging innovation, supporting infrastructure development, and offering financial incentives, proactive policies can create a viable path for SAF production using agriculture as the cornerstone feedstock supplier. Perhaps agriculture is part of the solution after all.

To find out more about this topic or to discuss our international agricultural advisory services, please contact our team using the link below.

Keep updated

Keep up-to-date with our latest news and updates. Sign up below and we'll add you to our mailing list.